Four Ways a Stablecoin Breaks, Reflexivity, Reserves, Redemption, and Contagion

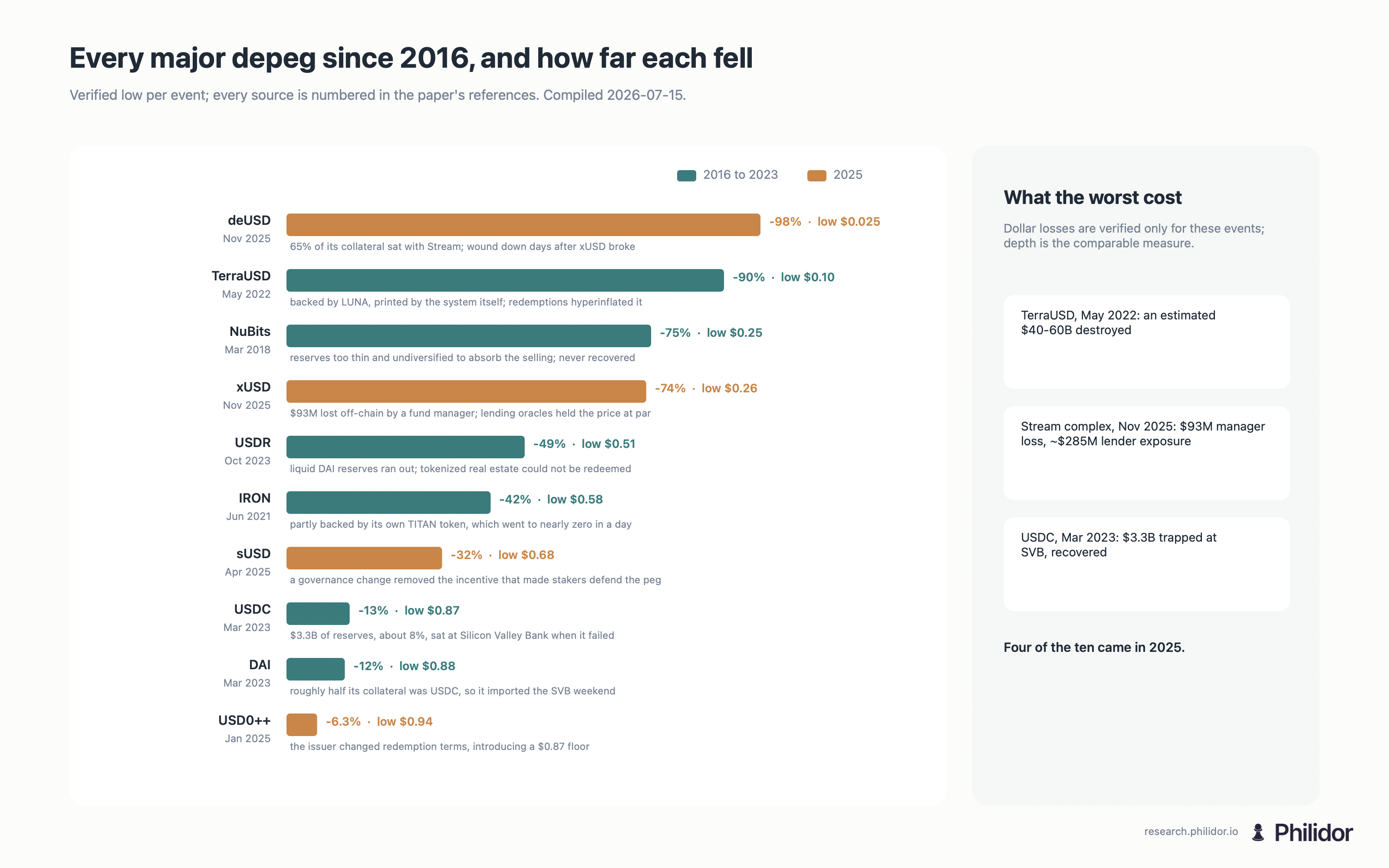

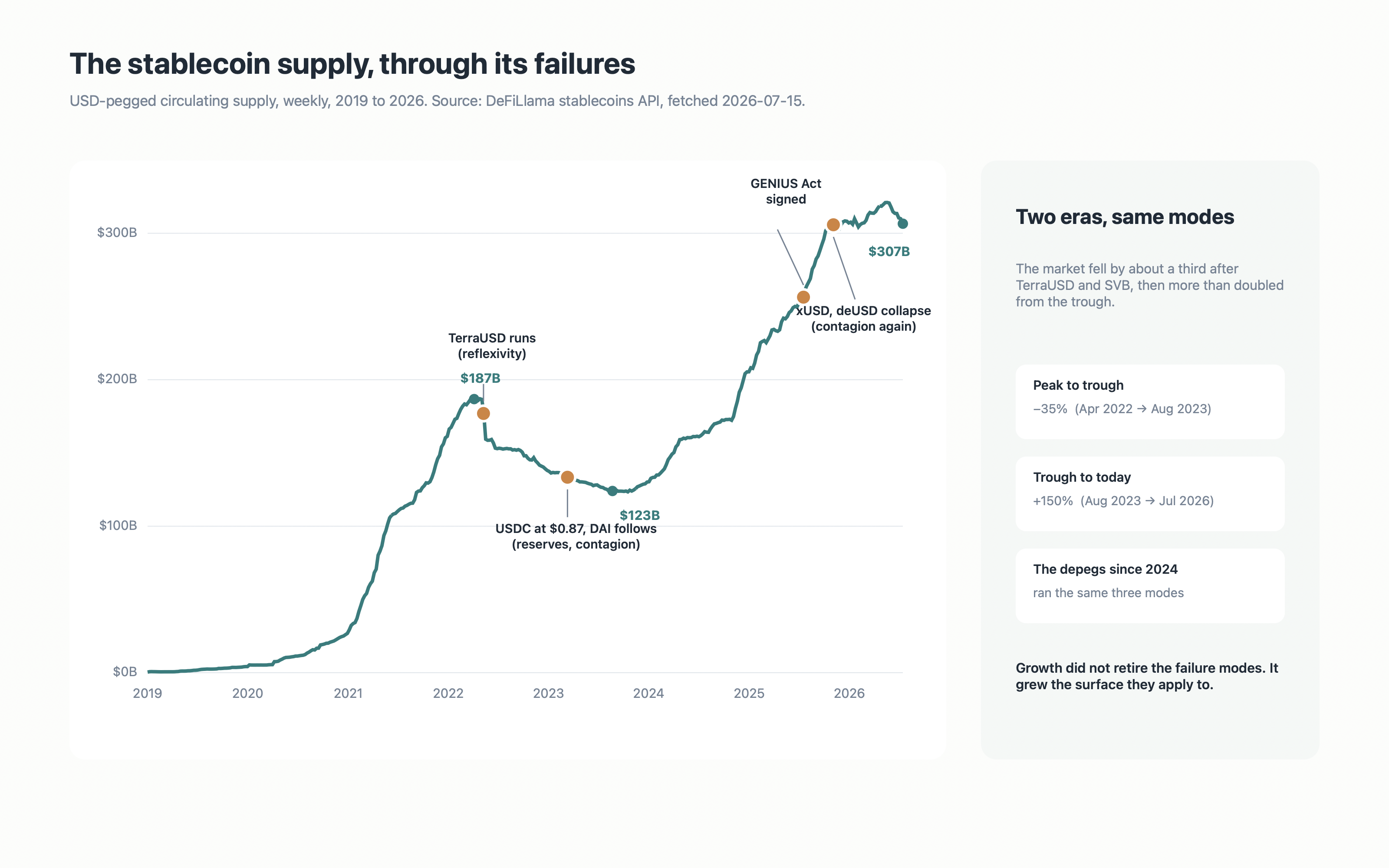

This casebook collects eleven major depegs since 2016, four of them in 2025 alone, two within months of the first federal stablecoin law being signed. A depeg is what happens when a coin that is supposed to trade at a dollar stops doing so. Major here names a selection rather than a census. It means USD coins large enough or integrated enough that their break mattered beyond their own holders, and that visibly traded below par, meaning below a dollar, on liquid venues. The committed catalog charts the ten breaks that have comparable recorded lows. The eleventh, the 2016 NuBits break, repegged after three months and has no comparable low. Basis appears only as a design precedent, because it shut down before launch. The mildest of last year's breaks stopped near $0.94. The worst ended at about two and a half cents. And the market running this experiment keeps growing, from a $122.7B trough in August 2023 to about $307B of USD-pegged supply by July 2026.1

Sort those eleven breaks by mechanism instead of by date and the mess collapses into four failure modes, each with its own warning signs and its own worst case. That sorting is the useful result. "Is it safe" has no static answer. The practical question about any stablecoin is which of the four ways it would break, and whether that mode is correlated with the rest of your book.

A decade of depegs, on one page

The supply chart reads like a stress test that keeps being rerun at larger size. About $4.2B of USD-pegged supply in January 2020 grew to a $187.4B peak in April 2022, fell by about a third to $122.7B by August 2023 after the TerraUSD and SVB shocks, then more than doubled from the trough to about $307B by July 2026.1 Growth did not retire the failure modes. Growth enlarged the surface they apply to. Here is the record, sorted by the dominant mode at the point of failure, with hybrids marked; one event can run a trigger in one mode and its amplifiers or transmission in another.

| Coin | When | Low | Mode | What broke |

|---|---|---|---|---|

| deUSD2 | Nov 2025 | ~$0.025 | Contagion | 65% of collateral one hop away, at Stream |

| xUSD3 | Nov 2025 | $0.26 | Reserves (trigger; contagion downstream) | Custody loss at its fund manager; 4× loop and par-pinned oracle amplified it |

| sUSD4 | Apr 2025 | $0.68 | Redemption / reflexivity (hybrid) | Peg-defence incentive removed by a design change |

| USD0++5 | Jan 2025 | $0.937, floor $0.87 | Redemption | Issuer changed the exit price under the peg |

| USDR6 | Oct 2023 | ~$0.51 | Redemption / reserves (hybrid) | Liquid redemption assets exhausted; illiquid real estate remained |

| DAI7 | Mar 2023 | ~$0.88 | Contagion | USDC in the peg-stability module |

| USDC8 | Mar 2023 | $0.87 | Reserves | $3.3B of reserves at a failed bank |

| TerraUSD | May 2022 | ~$0.10 | Reflexivity | Endogenous collateral, the full spiral |

| IRON9 | Jun 2021 | $0.58, settled ~$0.74 | Reflexivity | Partial backing by its own TITAN token; TITAN went to ~zero |

| NuBits10 | Mar 2018 | ~$0.25 | Reserves | Insufficient, undiversified reserves; the break was terminal |

| NuBits10 | Jun 2016 | repegged after 3 months | Reflexivity | Demand fled into a rising bitcoin; the defence was too slow |

| Basis11 | Dec 2018 | never launched | Reflexivity, avoided | Seigniorage design shut down pre-launch, $133M returned |

Two patterns stand out. The reflexive designs cluster early and have not returned at scale. The market learned that lesson expensively. And since TerraUSD, the reflexive mega-collapse of 2022, every break has run through reserves, exits, or collateral chains. That is the plumbing, and it grows with the market rather than with any single design.

The map was drawn before the failures

None of these modes surprised the research literature. The stablecoin design space reduces to two questions. Who holds the backing, an issuer with a bank account or a smart contract. And what the backing actually is. Klages-Mundt and coauthors drew that map in 2020 and named the distinction this paper leans on hardest.12 Exogenous collateral has value outside the stablecoin system, dollars in a bank, Treasury bills, ETH. Endogenous collateral is an asset the system itself creates to be its own backing, which means it can fail all the way to zero, because it is a claim on confidence in the very system under stress. The same authors modeled the deleveraging spiral in 2019 and 2020, two years before TerraUSD ran one live.1314

Among research desks, the closest prior treatment is S&P Global's 2023 study of depeg frequency and duration across five coins by collateral type.15 It rates issuers. No desk has sorted the full decade of failures by mechanism and then wired the result into live, coin-level scoring. That is what this paper adds.

| Mode | What fails | The tell, in advance |

|---|---|---|

| Reflexivity | The backing is confidence in the coin itself | Endogenous collateral; yield that funds the peg |

| Reserves | The backing is real but trapped or impaired | Concentrated custodians; opaque reserve reporting |

| Redemption | The path from coin to dollar narrows or closes | Few authorized redeemers; gated exits; changeable terms |

| Contagion | Another coin's failure arrives through the collateral | Stablecoins backing stablecoins; unresolved wrappers |

Mode one, contagion, the failure that arrives from next door

The freshest entries in the record sit on the contagion path, and the pair shows the difference between a trigger and a transmission. In early November 2025, Stream Finance disclosed that an external fund manager had lost about $93M. That was a reserve-custody failure rather than a contagion. Its synthetic dollar xUSD, which borrowed against its own collateral in a loop, fell 77% to $0.26 in a day. The fall was that steep because roughly 4× recursive leverage magnified the loss, while the price feed the protocol relied on kept quoting xUSD at a dollar.3 The clean contagion case is one hop away. Elixir's deUSD had parked 65% of its collateral with Stream, and when xUSD broke, deUSD fell more than 97% to about $0.025 and was wound down.2 deUSD's holders did nothing wrong by their own coin's lights. The failure arrived through the collateral.

The canonical precedent is DAI in March 2023. Overcollateralized, nominally decentralized, and it dropped to about $0.88 the same weekend USDC did,7 because roughly half of DAI's collateral entering 2023 was USDC,16 about $3 billion of it in MakerDAO's peg-stability module.17 The Federal Reserve's post-mortem named the channel in a sentence worth keeping. The peg module "worked as expected, just not as intended," creating not stability but a direct channel of contagion from USDC to DAI.18 MakerDAO debated emergency measures and voted to keep USDC anyway.17

A stablecoin collateralized by another stablecoin does not diversify the peg. It transmits it. That is why this mode grows with the market, the connective tissue of on-chain credit is far thicker than it was in 2018, and why look-through, tracing what backs the backing, is the only defence that works in advance. Our dependency-graph work exists to run that trace continuously.

Mode two, redemption, the exit narrows before the backing fails

Some breaks never involve bad backing at all. The exit itself fails. Tangible's USDR held real assets, but when redemptions exhausted its liquid DAI in October 2023, holders were left queued against tokenized real estate and the price fell to about $0.51 within hours.6 Usual's USD0++ broke in January 2025 when the issuer changed the redemption terms underneath the coin, introducing a $0.87 floor price, and the market repriced it to about $0.937 within a day.5 Synthetix's sUSD drifted to $0.68 in April 2025 after a governance change removed the incentive that had made stakers defend the peg.4

The research here is newer but sharp. Ma, Zeng and Zhang showed that par redemption is deliberately concentrated. Tether allows only 6 agents in an average month to redeem coins for cash. That design buys everyday price stability at the cost of amplified fragility when those few exits matter.19 The BIS makes the structural point in one line. What par settlement confronts is liquidity rather than solvency.20 A peg is a promise about an exit. Anything that narrows the exit, gates it, or reprices it is a failure mode of its own, whatever the reserves say.

Mode three, reserves, good backing in the wrong place

USDC is fully reserved in cash and short-dated Treasuries, and it broke anyway. In March 2023, Circle disclosed that $3.3 billion of reserves, roughly 8%, sat at Silicon Valley Bank, which had just failed.2122 By around 2am on 11 March, USDC traded at $0.87.8 How it recovered says as much as how it broke. USDC re-pegged when US regulators backstopped SVB depositors over the weekend and redemptions resumed on Monday 13 March,23 not through anything on-chain.

This is the oldest failure in finance wearing a new asset, the run Diamond and Dybvig formalized in 1983.24 The New York Fed later measured the crypto version and found stablecoins behave like money market funds under stress, with redemptions accelerating once the price breaks $0.99.25 NuBits ran a smaller version of the same mode in March 2018, when reserves that were insufficient and undiversified could not absorb the selling, and the coin settled near $0.25 for good.10 The lesson for scoring is that a peg is only as good as the weakest custodian of its backing, and that this mode can recover, because the assets exist, while the holder carries the mark-to-market pain in the meantime.

Mode four, reflexivity, the historical one

The mode that made depegs famous is now the rarest at scale. TerraUSD was its full expression, a peg defended by an arbitrage against LUNA, a token the system itself printed. When UST slipped below $1 in May 2022, the defence accelerated the collapse, LUNA's supply hyperinflated from roughly 350 million to over 6.5 trillion tokens in days, UST bottomed near $0.10, and an estimated $40 to $60B evaporated. The forensics found a few large holders repositioned first and that the blockchain's transparency let everyone watch everyone else exit, which sped the run up.26 It was also the third run of the same experiment. NuBits broke in 2016 when its defence proved too slow for a demand rush.10 Basis shut down in December 2018 before launch and returned $133M.11 Iron Finance's IRON, partially backed by its own TITAN token, collapsed in June 2021 in what its own post-mortem called the first large-scale crypto bank run.927

The design literature had this mode mapped in advance, a peg backed by endogenous collateral has no floor from the outside.14 The market appears to have absorbed that lesson, no new large-scale algorithmic peg has launched since. The reason to keep the mode on the map is subtler. Reflexivity survives in fragments, inside coins whose headline design looks nothing like Terra. A loop here, as when xUSD ran roughly 4× recursive leverage. An incentive dependency there, as with sUSD.

The common thread is concentration meeting correlation

Read together, the record shows why a stablecoin failure is rarely contained to the coin that failed.

- Concentration. A small number of coins back the majority of on-chain credit, so a single failure is large. USDT and USDC alone are about 83% of the $310B stablecoin supply (DeFiLlama, 2026-07-08).

- Correlation. The failure modes are linked. DAI was tied to USDC through collateral. The whole fiat-backed class shares the same banking rails. The 2025 synthetic dollars shared the same lending-market plumbing.

A portfolio that spreads money across vaults but holds USDC, DAI, and a third USDC-collateralized coin is not diversified against the risk that matters. Those are three expressions of one banking-reserve exposure. The thing that actually reduces risk is spreading across the failure modes, not the issuer brands.

What the new rules reach, and what they leave open

The GENIUS Act, signed 18 July 2025, requires payment stablecoins to hold reserves on an at least 1 to 1 basis in cash, insured deposits and Treasury bills of 93 days or less, to publish reserve composition monthly, to forgo paying holders interest, and not to lend the reserves out again.2829 It also reaches redemption inside its perimeter. Permitted issuers must publicly disclose a redemption policy with clear and conspicuous procedures for timely redemption, may impose discretionary limits only under regulator authority, and must give at least seven days' notice before changing redemption fees.28 Read against the four modes, the repair is real but bounded twice over. The first bound is the perimeter. The Act governs payment stablecoins, meaning digital assets designed for payment or settlement that their issuer must redeem at fixed value. It separately bars permitted issuers from paying holders interest or yield. The November 2025 failures, xUSD and deUSD, were synthetic dollars built to deliver yield. They are products the permitted regime is designed not to license, rather than instruments that failed inside it, and neither had any path to permitted status. The second bound is timing. The Act's obligations phase in after enactment rather than arriving at signature, so no part of the November episode ran under an operative regime. Inside the perimeter, it effectively outlaws endogenous backing, closing reflexivity, and it standardizes reserves onto short government paper and insured rails, safer, though the rail dependence the SVB weekend exposed is now institutionalized rather than removed.

Collateral contagion is the mode the Act touches least, in two very different ways. Inside the perimeter, its eligible-reserve rules keep ordinary stablecoins out of a permitted issuer's backing, which closes the DAI-style channel there. Outside it, nothing in the Act reaches the collateral chains of synthetic dollars, and that is exactly where the November 2025 contagion ran, within four months of signature. None of this is new in the history of money. Gorton and Zhang argued that privately issued money has never held par on its own, only under regulation or insurance.30 The Fed's own history of the banknote era adds the detail that matters for scoring. Notes backed by better collateral saw shallower discounts in stress.31 The table above is the same phenomenon with block explorers.

Implications for risk scoring

The four modes map directly onto how a peg should enter a risk model.

- Classify by failure mode, not by name. The modes have different worst cases and different warning signs. Philidor's methodology separates synthetic and fiat-backed stablecoin classes for exactly this reason, the class determines the shape of the failure. This takes the exogenous and endogenous split from the design literature and turns it into something a risk model can act on.

- Score the peg as a live input, not a static label. A coin is at $1.00 today and could be at $0.87 tomorrow. The decline is not gradual either. Redemptions accelerate once the price breaks the $0.99 threshold the New York Fed estimated.25 Philidor runs live peg monitoring for stablecoin-class assets, with a cooldown and automatic recovery once the coin re-pegs.

- Look through to collateral. A stablecoin backed by other stablecoins inherits their failure modes. Our asset vector, the part of Philidor's scoring that tracks what a coin is backed by, has to score what backs the backing. DAI proved it in 2023 and deUSD reproved it in 2025, at a worse exchange rate.

Peg events are continuous, not occasional. Recent critical incidents across the tracked universe, overwhelmingly depeg events, make the point.

What to ask before a coin becomes the safe part of your portfolio

Five questions, one per failure mode and one for the portfolio. Each maps to a failure channel that at least one break in the table ran; they are diligence prompts, not a guarantee of advance warning.

- Who can redeem at par, and how many entities is that in practice? Six agents in an average month is a very different peg than open redemption, and redemption terms that governance can change are a mode of their own.

- Is the backing exogenous, endogenous, or mixed? Can it be marked independently of the system that issued it?

- Where do the reserves physically sit, and what fails alongside them? A bank, a Treasury account, a smart contract, a fund manager.

- What backs the backing one hop down? DAI answered this badly in 2023 and deUSD in 2025. Our dependency-graph work answers it continuously.

- How much of the rest of your stablecoin book gives the same answers? Diversification across brands that share one failure mode is one exposure wearing several logos.

TerraUSD failed because its peg had no floor from the outside. USDC wobbled because its floor sat in a failing bank. USD0++ repriced its own exit. DAI and deUSD dropped because their floor was someone else's coin. Four modes, one lesson. Price the mechanism and the collateral path, monitor the peg as a live signal, and treat the issuer brand as the least informative thing in the set.

References

-

DeFiLlama (2026). Stablecoins API, total USD-pegged circulating supply. Accessed 2026-07-15. Weekly series committed at /data/stablecoin-depeg-failure-modes/stablecoin-supply-weekly.json. ↩ ↩2

-

Bashir, K. (2025). Elixir Shuts Down deUSD Stablecoin After Stream Finance's $93 Million Loss. BeInCrypto via Yahoo Finance. Accessed 2026-07-15. ↩ ↩2

-

Vismaya, V. (2025). Stream Finance Stablecoin Plunges 77% After Protocol's Fund Manager Loses $93 Million. Decrypt. Accessed 2026-07-15. ↩ ↩2

-

Cointelegraph (2025). Synthetix's sUSD stablecoin continues fall after depeg, tapping $0.68. Via TradingView. Accessed 2026-07-15. ↩ ↩2

-

Collymore, H. (2025). USD0++ loses 1:1 USD peg, panic reigns. Cryptopolitan. Accessed 2026-07-15. ↩ ↩2

-

Reynolds, S. (2023). Real Estate-Backed Stablecoin USDR De-Pegs After Treasury Was Drained of Liquid Assets. CoinDesk. ↩ ↩2

-

CoinDesk (2023). DAI Depegs to Lifetime Lows as Stablecoin Rout Plagues Crypto. ↩ ↩2

-

Chainalysis (2023). Crypto's Reaction to the Demise of Silicon Valley Bank and Its Impact on USDC. Chainalysis blog. Accessed 2026-07-15. ↩ ↩2

-

Iron Finance (2021). Iron Finance Post-Mortem 17 June 2021. Medium. Accessed 2026-07-15. ↩ ↩2

-

Reserve Research Team (2018). The End of a Stablecoin, The Case of NuBits. Reserve blog. Accessed 2026-07-15. ↩ ↩2 ↩3 ↩4

-

Dale, B. (2018). Basis Stablecoin Confirms Shutdown, Blaming 'Regulatory Constraints'. CoinDesk. ↩ ↩2

-

Klages-Mundt, A., Harz, D., Gudgeon, L., Liu, J.-Y. & Minca, A. (2020). Stablecoins 2.0: Economic Foundations and Risk-based Models. ACM Advances in Financial Technologies. ↩

-

Klages-Mundt, A. & Minca, A. (2019). (In)Stability for the Blockchain: Deleveraging Spirals and Stablecoin Attacks. arXiv. ↩

-

Klages-Mundt, A. & Minca, A. (2020). While Stability Lasts: A Stochastic Model of Non-Custodial Stablecoins. Mathematical Finance (2022). ↩ ↩2

-

S&P Global (2023). Stablecoins: A Deep Dive into Valuation and Depegging. S&P Global special editorial. ↩

-

Sandor, K. (2023). Stablecoin Issuer MakerDAO Votes to Retain USDC as Primary Reserve Even After Depeg. CoinDesk. ↩ ↩2

-

Du, C., Sonawane, R. & Watsky, C. (2025). In the Shadow of Bank Runs: Lessons from the Silicon Valley Bank Failure and Its Impact on Stablecoins. FEDS Notes, Federal Reserve Board. ↩

-

Ma, Y., Zeng, Y. & Zhang, A. L. (2025). Stablecoin Runs and the Centralization of Arbitrage. NBER Working Paper 33882. ↩

-

Aldasoro, I., Mehrling, P. & Neilson, D. H. (2023). On par: A Money View of stablecoins. BIS Working Papers No 1146. ↩

-

CNBC (2023). Stablecoin USDC breaks dollar peg after firm reveals it has $3.3 billion in SVB exposure. ↩

-

CoinDesk (2023). Circle Confirms $3.3B of USDC's Cash Reserves Stuck at Failed Silicon Valley Bank. ↩

-

CoinDesk (2023). USDC Stablecoin Regains Dollar Peg After Silicon Valley Bank-Induced Chaos. ↩

-

Diamond, D. W. & Dybvig, P. H. (1983). Bank Runs, Deposit Insurance, and Liquidity. Journal of Political Economy 91(3). ↩

-

Anadu, K. et al. (2023). Runs and Flights to Safety: Are Stablecoins the New Money Market Funds? Federal Reserve Bank of New York Staff Reports, No. 1073. ↩ ↩2

-

Liu, J., Makarov, I. & Schoar, A. (2023). Anatomy of a Run: The Terra Luna Crash. NBER Working Paper 31160. ↩

-

The Defiant (2021). Iron Finance Implodes After 'Bank Run'. Accessed 2026-07-15. ↩

-

119th Congress (2025). GENIUS Act, Public Law 119-27. U.S. Government Publishing Office. ↩ ↩2

-

Congressional Research Service (2025). Stablecoin Legislation: An Overview of S. 1582, GENIUS Act of 2025. CRS Insight IN12553. ↩

-

Gorton, G. B. & Zhang, J. Y. (2023). Taming Wildcat Stablecoins. University of Chicago Law Review 90(3). ↩

-

Carlson, M. (2026). A brief history of bank notes in the United States and some lessons for stablecoins. FEDS Notes, Federal Reserve Board. ↩